Time: 2023-10-09

Time: 2023-10-09  Views: 692

Views: 692

[Foreword]

The reason why Decision is highly praised by enterprises during the implementation of digital transformation projects is because experts are escorting Decision during the project process to help enterprises gain new knowledge, grow new capabilities, and improve management during the implementation of digital transformation projects. To improve our vision and reduce project misunderstandings, we have specially set up a "Decision Expert Column" to share with you a series of articles on the implementation of digital transformation projects, so stay tuned.

This article is based on Mr. Yang Yongqing, Decision’s chief financial expert, who has 24 years of rich experience in the field of SAP ERP, and combines the common misunderstandings he found in the implementation of ERP projects to publish corresponding research insights and suggestions to protect your SAP financial implementation and delivery.

[Problem Description]

What is the consumption (Consumption) in the allocation cycle Cycle proposed by the user, and what is the role of the selection?

[Problem analysis]

There are two places in the allocation amortization cycle where there is consumption (Consumption):

① In the cycle header (only applicable to allocation, not apportionment);

② In the drop-down selection on the first page of segment information (applicable to allocation allocation).

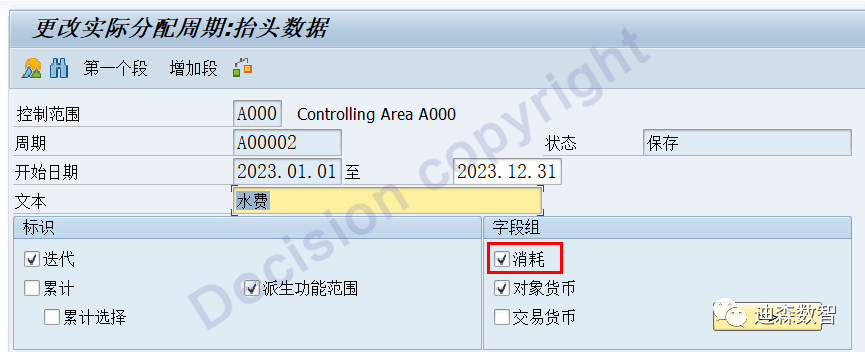

- Consumption in the Cycle header (Consumption)

After selection, the sender not only sends the cost amount, but also the corresponding consumption quantity.

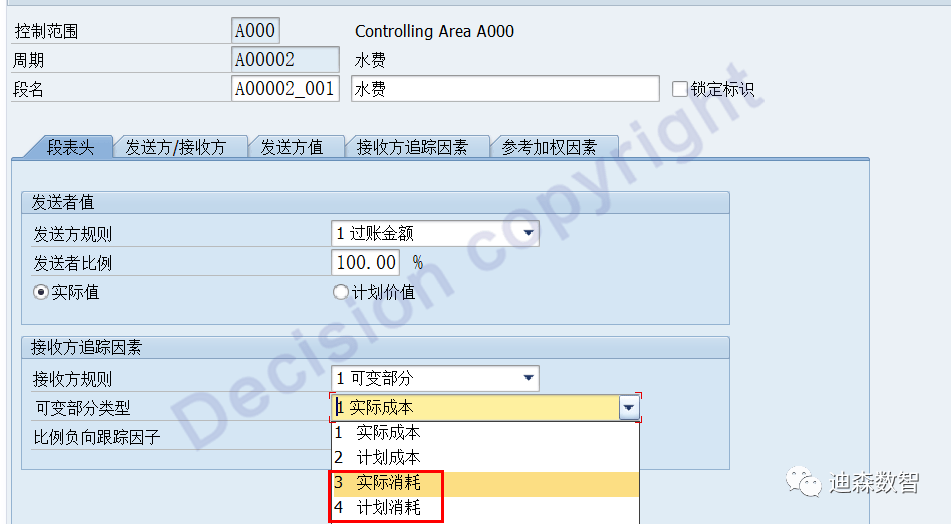

-Consumption of the drop-down selection items on the first page of segment information (Consumption)

After selection, the receiver will allocate the base rate based on the consumption quantity in the specified account.

[Detailed demonstration]

① Consumption in the Cycle header (only applicable to allocation, not apportionment)

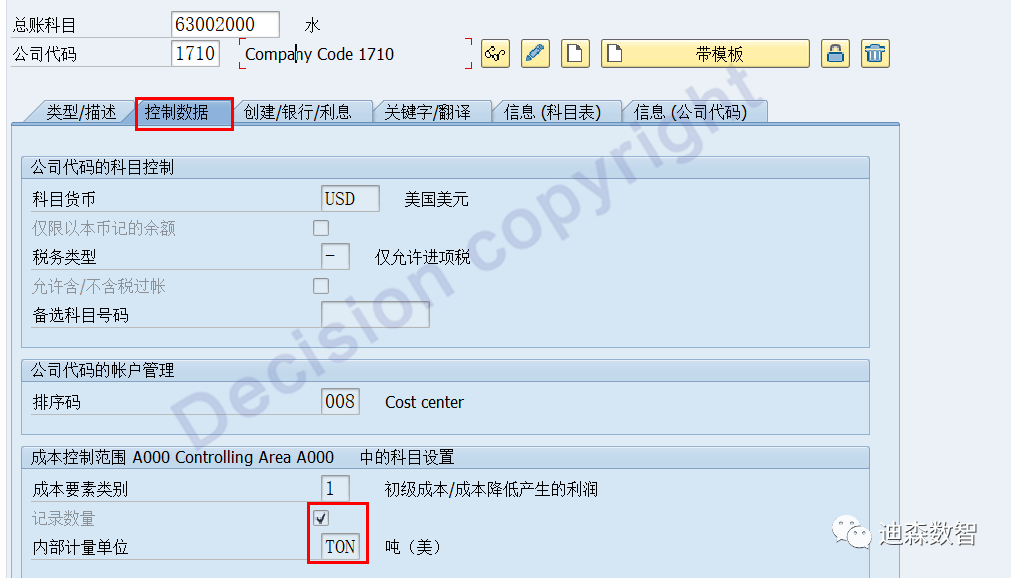

1.1 The primary cost element master data of the sender's accounting. The following figure takes the water fee account as an example:

The corresponding primary cost element must be checked: record the quantity and specify the unit of measurement, such as water fee: TON

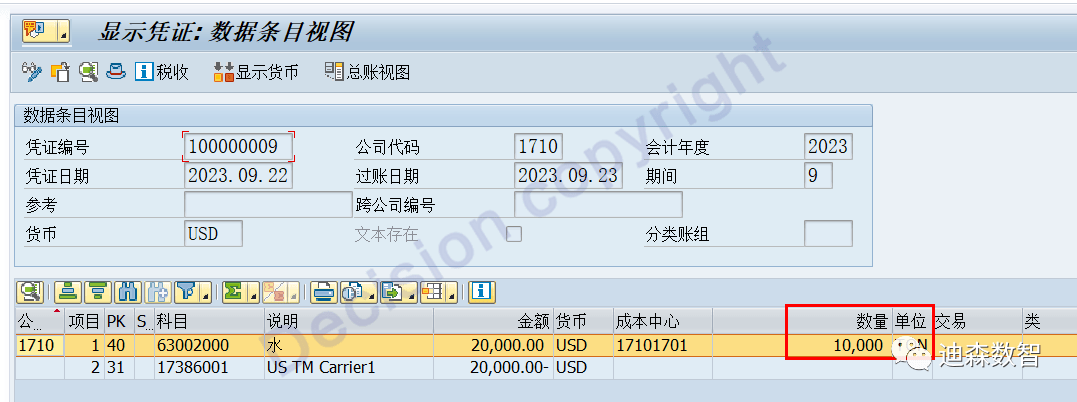

1.2 When recording primary cost element accounts, enter the amount of 20,000 USD and the quantity of 10,000 TON, and the measurement unit is the same as the cost element master data unit:

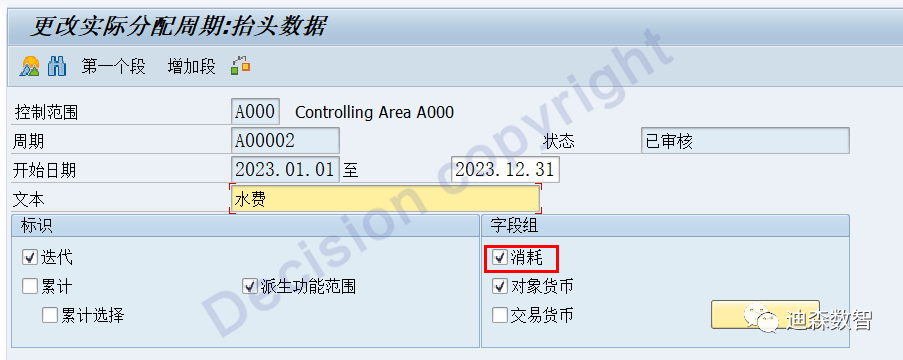

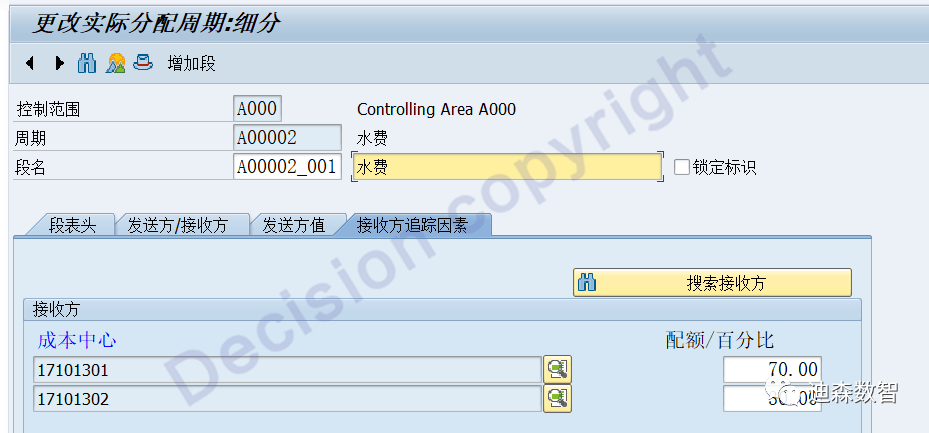

1.3 During cycle maintenance, the simultaneous allocation - quantity is specified in the header information:

Assume that the two receivers receive 70% of the cost and 30% of the cost:

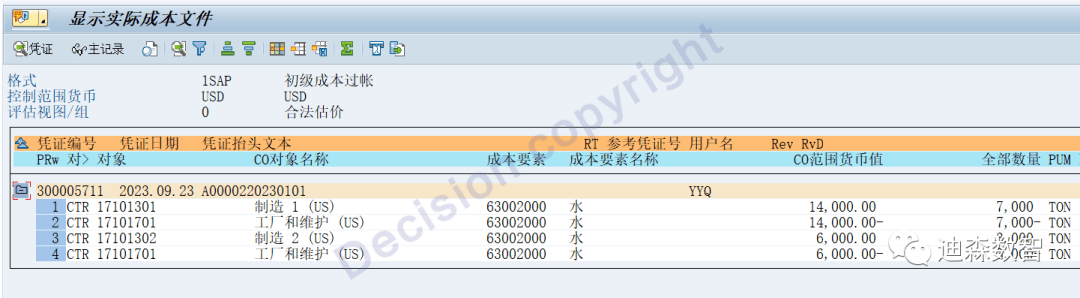

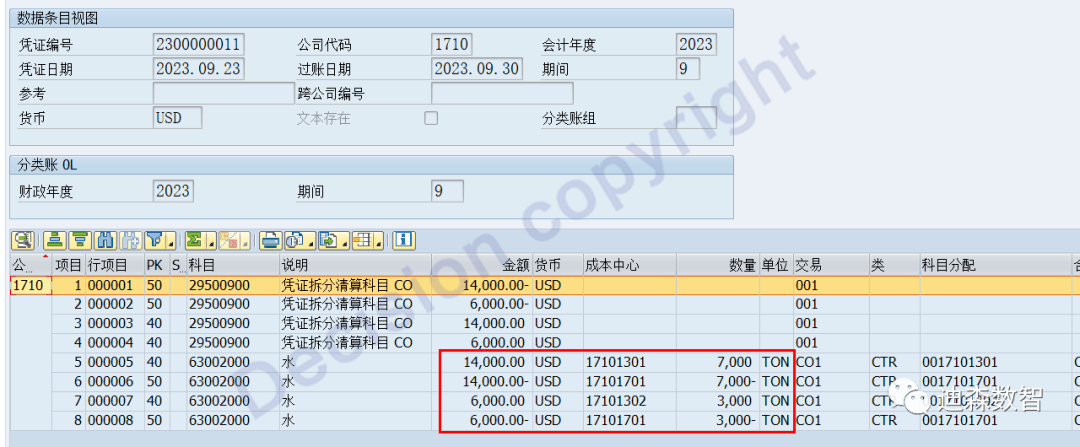

1.4 After the Cycle is executed, the cost amount and quantity allocated at the same time can be seen in the CO voucher and FI voucher.

② In the drop-down selection on the first page of segment information (applicable to allocation allocation)

2.1 There are no special requirements for the primary cost element/secondary cost element master data of the sender's accounting;

2.2 When recording primary cost elements/secondary cost elements, there are no special requirements for quantity records;

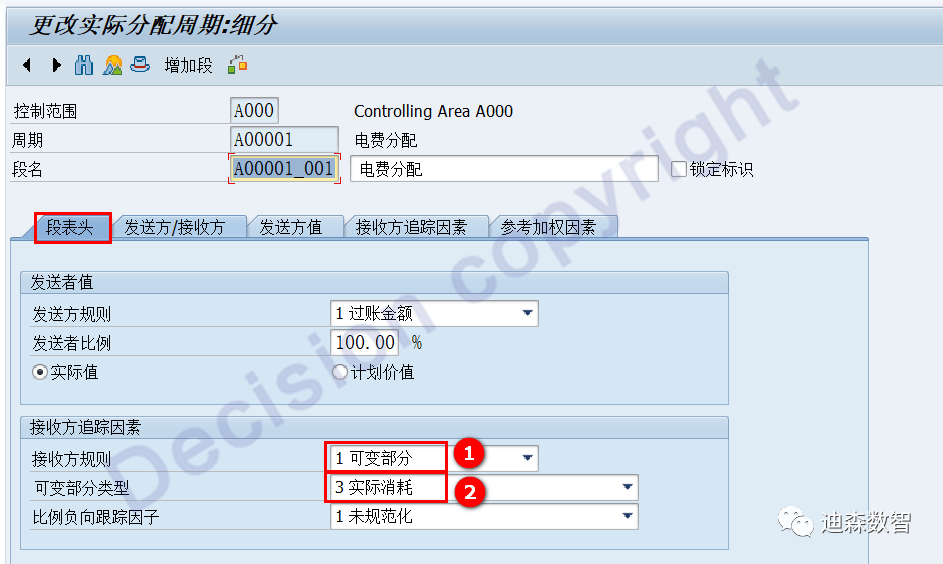

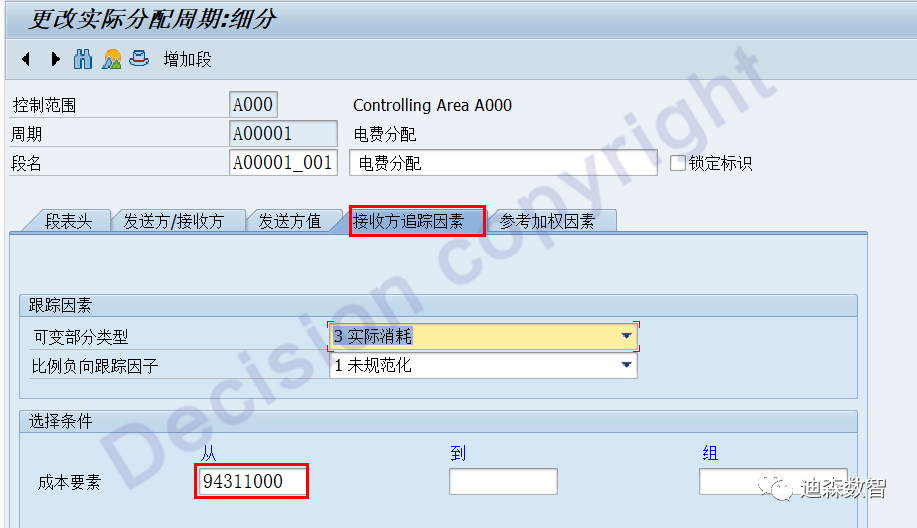

2.3 During cycle maintenance, pull down the first page of segment information and select:

First select: variable base ratio, then select: according to actual consumption quantity

Assume that allocation is based on the quantity of the cost element of the recipient: 94311000

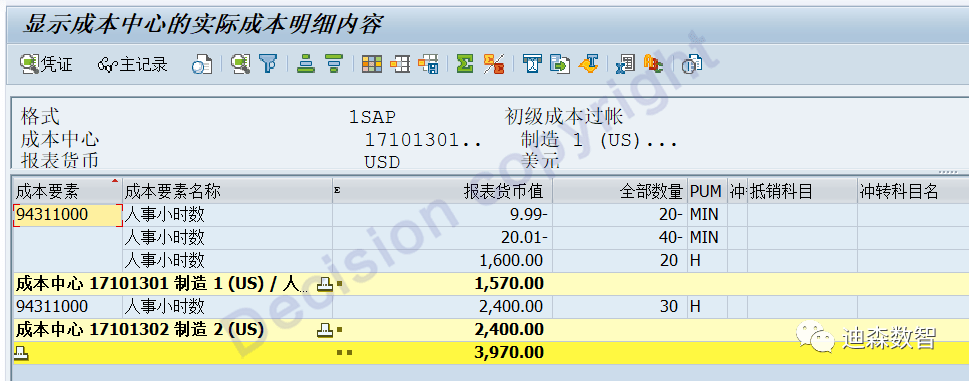

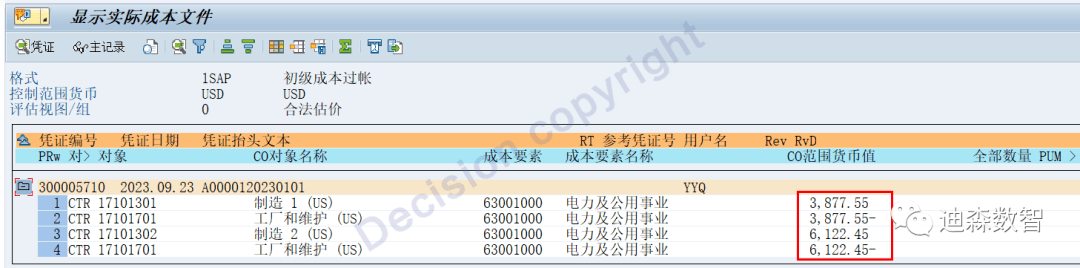

2.4 Receipt: 94311000 The quantity of cost elements is as follows: Transaction code KSB1 query:

Cost center: 17101301 hours quantity = (-20MIN) + (-40MIN) + 20 hours = 19 hours

Cost center: 17101302 hours quantity = 30 hours

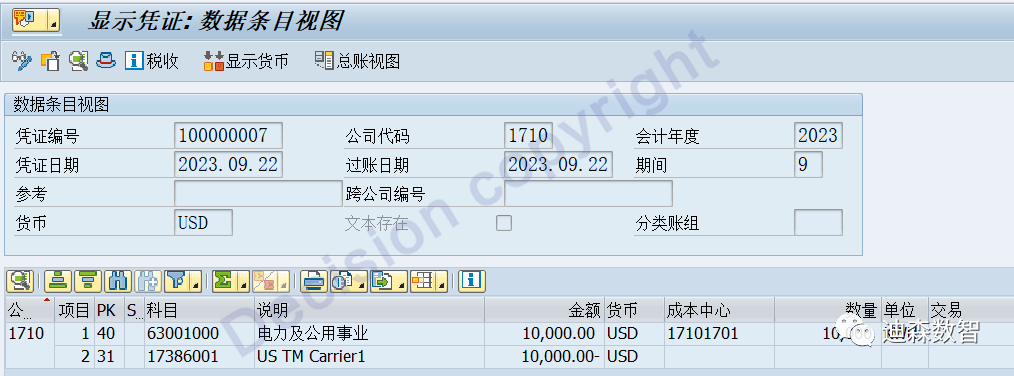

2.5 The sender’s cost element accounting is as follows: 10000USD

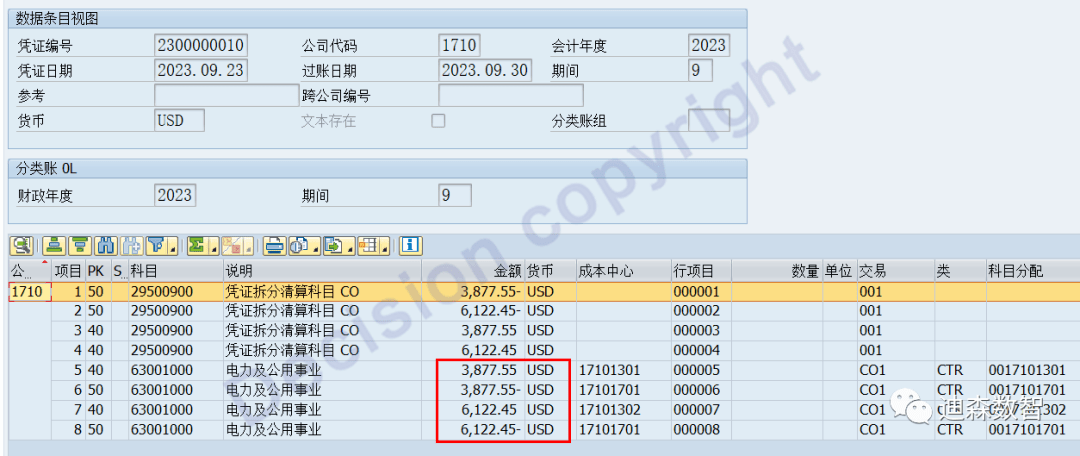

2.6 After the Cycle is executed, the cost amount allocated at the same time can be seen in the CO voucher and FI voucher.

Cost center: 17101301 commitment = 19 * 10000/(19+30) = 3877.55

Cost center: 17101302 commitment = 30 * 10000/(19+30) = 6122.45

Note: For the allocation cycle Cycle, you can select at the same time: select Consumption in the Cycle header; select Actual Consumption or Plan Consumption in the drop-down selection on the first page of the segment information.

If you would like to ask more questions and needs about digital transformation projects and learn more about Decision’s innovative solutions, you are welcome to contact Decision and we will answer your questions.

Consultation hotline: 400-600-8756

WeChat: Decision_SAP

Email: public@decision-it.com

Note: This article is the original work of Yang Yongqing. No individual or institution may reproduce or quote large sections for commercial purposes without his consent.

【Service Guide】

For more information on SAP courses, project consultation and operation and maintenance, please call Decision's official consultation hotline: 400-600-8756

【About Decision】

Global professional consulting, technology and training service provider, SAP gold partner, SAP software partner, SAP implementation partner, SAP official authorized training center. Seventeen years of quality, trustworthy!